Category: Government

-

The New Police Tech Tracking Your Phone, Car, Pet Chip, errr… Everything Electronic

License plate cameras just leveled up, and they see your phone. If you own a car and are concerned about privacy, this is for you. There is a massive story pertaining to privacy centered on your car and its license plate, but that opens the door to all of your electronics and you being tracked.…

-

The Silent Revolution: Scaling the CIA’s AI Frontier

In the hushed, high-stakes corridors of the Special Competitive Studies Project (SCSP) summit, Michael Ellis, Deputy Director of the Central Intelligence Agency (CIA), delivered a briefing that felt less like a standard government update and more like a tech keynote from the bleeding edge. As a technologist, listening to Ellis, the youngest person to ever…

-

SCSP Summit Dispatch: Securing the Future in the Age of Agentic Intelligence

The technological landscape is shifting beneath our feet, moving from a period of digital assistance to an era of Agentic AI, systems capable of not just processing information, but executing complex goals with minimal human intervention. At the recent Special Competitive Studies Project (SCSP) session, “AI and The Future of Global Security,” the conversation transcended…

-

The AI Sieve and the Drone Epidemic: Lessons from the Israeli Battlespace

At the recent Special Competitive Studies Project (SCSP) summit, the focus shifted from domestic policy to the jagged edges of active conflict. Dr. Eyal Hulata, former Israeli National Security Advisor and former head of the Mossad’s technology division, joined Michael Allen of Beacon Global Strategies for a session that was part tactical briefing, part futurist…

-

Ready for the Future of AI and Politics? Gary F. Bengier, Writer, Philosopher & Technologist

Gary is a famous Silicon Valley Technologist (he’s the former eBay CFO!) and Philosopher with a fascinating & well informed view on the future of AI & Politics. Today we will hear his pearls of wisdom as he shares insights and actionable advice about the future of AI and the challenges humans will face in…

-

The Future of Geopolitics and the Role of Innovation and Technology

Washington, D.C., Walter E. Washington Convention Center – In the whirlwind world of technology and geopolitics, the recent panel discussion on “The Future of Geopolitics and the Role of Innovation and Technology” offered a fascinating blend of perspectives from esteemed experts, including Alex Karp, Cofounder and CEO, Palantir; David S. Cohen, Deputy Director Central Intelligence…

-

Dubai World Government Summit – Future Technology and its Impact on Regulation

Dubai, UAE – It was a pleasure and an honor to have been invited back to Dubai, and speak in front of their Excellencies and part of the Royal Family. I presented on several technologies that governments around the world will have to think about over the course of the next several years. These will…

-

Tech Snippets Today – Garry Kasparov – Chess Grandmaster

In the speaker’s green room at the Consensus 2022 conference, Garry Kasparov, Chess Grandmaster, and I caught up. This covers all things cryptocurrency and his belief in the importance of the technology to create more freedom for people across the world, especially in areas with more authoritarian regimes. For more information, please visit the following:…

-

Podcast: The Hearing – Stan Litow, Professor Duke and Columbia University

From the producer… The achievements of this episode’s guest have been celebrated by the Council on Foreign Relations, Harvard Business Review, The Economist, The New York Times, Forbes and Wired. Joe is talking to the founder of P-TECH, and author of Breaking Barriers, Stan Litow. They begin by discussing Stan’s early career – working for…

-

Podcast: The Hearing – Chris Mohr – VP for Intellectual Property and GC at SIIA

This week we talk privacy, piracy, and intellectual property. Before the lockdown, I sat down with Chris Mohr, VP for Intellectual Property and GC at Software and Information Industry Association. Working at the heart of the US federal government in Washington DC, Chris tells us about life as a lobbyist on Capitol Hill and how…

-

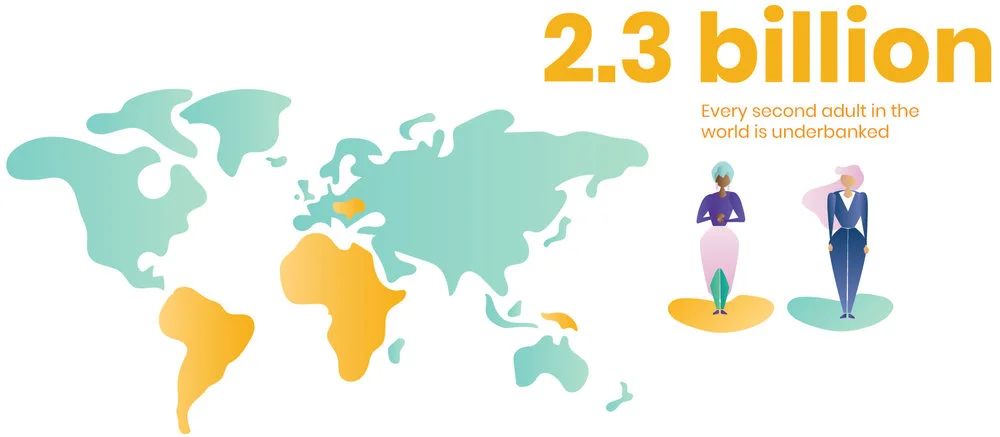

How technology is ridging the financial inequality gap for the unbanked

Originally published on AnswersOn. By Gina Jurva – Joseph Raczynski The Covid-19 pandemic is exposing long-standing societal inequalities that range from access to healthcare to access to childcare and place our society is under a microscope. One of the biggest challenges is getting stimulus funds to those who need it most, especially in those cases where the…

-

Part 2: Legal Geek’s Uncertain Decade: Can ALSPs provide what their clients want & need?

Originally published on AnswersOn. By Joseph Raczynski General counsel (GCs) across the United States and the United Kingdom have varied approaches to the current market conditions, according to recent surveys. Interestingly, at the center of the debate is how alternative legal service providers (ALSPs) are utilized and perceived compared to traditional law firms. Not surprisingly,…

-

The 4th Annual Government Day: The Reality and Skepticism of Innovation and Blockchain

Originally published on the Legal Executive Institute By Joseph Raczynski WASHINGTON, D.C. — The Government sector strives to ramp up its efforts to more widely integrate cutting edge technologies like blockchain, artificial intelligence, and the Internet of Things (IoT), it is running into a myriad of challenges. Not the least among them, is separating the…