Quantum computing is notorious for being both the most hyped and the most misunderstood sector in tech. At the recent Quantum.Tech event at the Conrad Hotel in Washington, DC, Michael Bogobowicz, Partner at McKinsey & Company, delivered a keynote that cut through the noise, offering a data-driven snapshot of where quantum stands today, and where it’s heading.

The Quantum Economy: From Winter to a Budding Spring

Recently, the quantum sector was deep in what Bogobowicz called a “quantum winter”, a period marked by a 23% decline in overall funding, as investors across tech tightened their belts. But 2025 has brought a thaw: funding is up 18%, and quantum investment volumes are still about 12% higher than most other tech categories. In other words, while AI might be hogging the headlines, quantum is quietly regaining its stride, with approximately $2 billion in annual investments now flowing into the sector.

A Surge of Big Tech and Startups

The last 12 months have seen a parade of major tech players stepping out of stealth mode and into the quantum spotlight. Google, Amazon (with its Ocelot chip), IBM, and Microsoft (with its Majorana chip) have all made significant announcements, signaling that the quantum arms race is no longer just for startups and academic labs. Nvidia, not to be left out, is also making moves in the space. These entries have been accompanied by “10x improvements” in error correction and hardware roadmaps, with some startups boasting dramatic leaps in performance and reliability.

Commercialization: Quantum’s Coming-of-Age Moment

Perhaps the most bullish news: revenues in quantum are rapidly catching up to investments. While the sector isn’t quite at the point where revenue eclipses investment, it’s getting close, a key sign of market maturity. Bogobowicz predicted that by 2025, the industry could cross the $1 billion mark in annual revenues, and within a year or two, revenues may finally outpace investments. For a field long dependent on hope and government grants, this is a major milestone.

The Rise of Global Innovation Hubs

Quantum isn’t just a Silicon Valley story. Around 20 to 30 innovation hubs are now active worldwide, from Maryland (where the state government has pledged $1 billion in funding) to Europe and Asia. These hubs are becoming magnets for talent, capital, and commercial use cases, often anchored by leading universities and fueled by a mix of public and private investment.

Talent: The Great Quantum Bottleneck

Despite all the investment, talent remains in critically short supply. The sector needs roughly twice as many quantum specialists as are currently available. Universities are ramping up, with 195 institutions now hosting quantum research groups and 55 offering dedicated master’s programs, a 10% increase year-over-year, but the gap remains daunting.

Technological Milestones: Error Correction and Beyond

The past year has seen breakthroughs in error correction, a crucial step toward scalable, fault-tolerant quantum computers. Companies like Microsoft and Quantinuum have demonstrated logical qubits with error rates 800 times better than physical qubits, and new architectures are reducing the hardware overhead needed for robust quantum computation. Meanwhile, advances in quantum communication (e.g., longer-distance quantum key distribution) and sensing (e.g., ultra-sensitive measurement devices) are expanding the field’s reach.

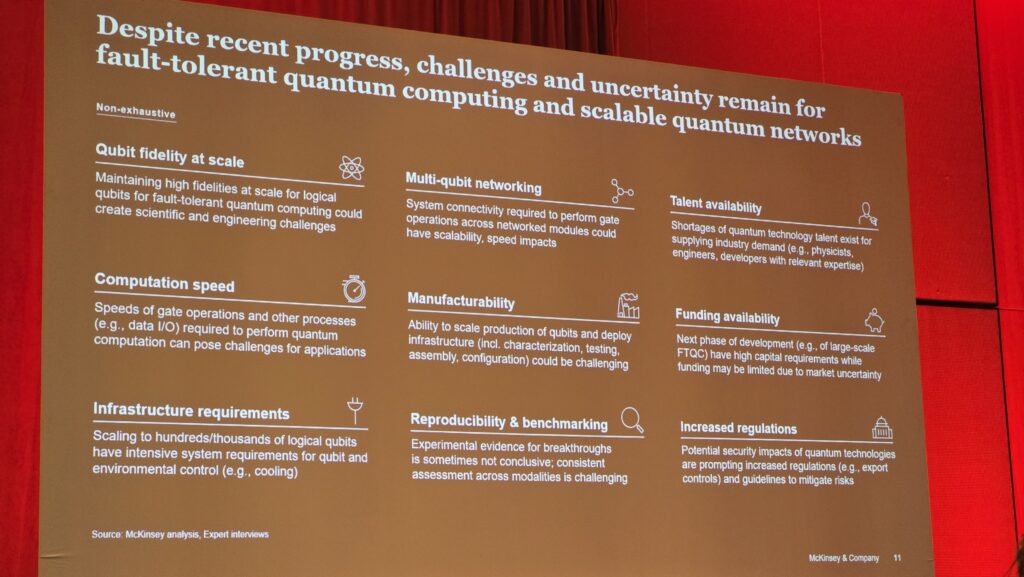

Challenges on the Horizon

It’s not all smooth sailing. Key uncertainties remain:

- Technical: Can we maintain qubit fidelity at scale? Will multi-qubit networking work as hoped?

- Workforce: Can the talent pipeline keep pace with demand?

- Manufacturing: Will we be able to scale up production of quantum hardware?

- Policy: How will export controls, regulation, and international collaboration evolve, especially as quantum nationalism heats up?

- Funding: Will public and private investment continue at current levels, or will there be another pullback as the sector matures?

The Quantum Value Proposition

Looking ahead, McKinsey projects that quantum technologies could generate $1–2 trillion in value by 2040, with sectors like chemicals, life sciences, finance, and mobility reaping the earliest and largest rewards. Quantum computing alone could account for $450 billion annually by 2035, with quantum sensing and communication contributing another $100–200 billion and $50–100 billion, respectively.

My Commentary: The Quantum Zeitgeist

If last year was quantum’s “winter,” this year feels like the first day of spring, muddy, unpredictable, but undeniably full of new shoots. The sector’s resilience is remarkable: even after a funding freeze, quantum is attracting both fresh capital and heavyweight entrants. The talent crunch is real, but so is the sense of urgency among universities and governments to fill the gap.

The message from Bogobowicz and McKinsey is clear: quantum is no longer a science experiment, it’s becoming a business, with real revenues, real customers, and real impact on the horizon. The next few years will be critical as the sector races toward fault tolerant machines and broader commercial adoption. As for the skeptics waiting for another “quantum winter,” they might want to invest in a pair of sunglasses, because this spring could get very bright, very quickly.

In quantum, as in life, the only constant is uncertainty. But if the last year is any indication, the industry is learning to thrive on it.

For more information, please visit the following:

Website: https://www.josephraczynski.com/

Blog: https://joetechnologist.com/

Podcast: https://techsnippetstoday.buzzsprout.com

LinkedIn: https://www.linkedin.com/in/joerazz/

Leave a Reply

You must be logged in to post a comment.